Biocon Ltd is the largest and fully-integrated biopharmaceutical company in India. The company has developed and taken a range of novel biologics, differentiated Small Molecules, biosimilar, affordable Recombinant Human Insulin, and analogues from logs to market. The company operates under 3 strategic segments Biologics, small molecules and research and development services. The company is 4th largest insulin producer in India. Furthermore, the company has a large portfolio of biosimilars under global clinical development commercialized in the developed markets i.e. The UK, the US and Japan. Some of the key brands of the company are INSUGED (RH-insulin), CANMAB (Trastuzumab), ALZUMAb (Itolizumab), KRABEVA (Bevacizumab), Basalog One (prefilled glargine pen), and BIOMAB-EGFR (Nimotuzumab).

Market Data:

| CMP | Rs. 621.25 |

| BSE Code | 532523 |

| NSE Code | BIOCON |

| Market CAP | Rs. 37,236 Cr. |

| 52 Week High | Rs. 718.35 |

| 52Week Low | Rs. 543.30 |

- Net profit: Rs. 214crores

- P/E: 42.36x

- ROE: 13%

- ROA: 4%

- EPS: 15.20

- ROCE: 41%

- ROIC: 9%

- EV/EBITDA: 88.12x

- R&D as % of sales: 17%

Financial for the year 2017-18

- Revenue from operations for Q4FY19 stood at Rs1, 528.8 crores as compared to Rs. 1,169.5 crores in Q4FY18. It increased by 31% on a YoY basis. The growth was led by the biologics segment (contributes 28% to total revenues), it grew by 87% on a YoY basis from Rs. 241 crores in Q4FY18 to Rs. 451 crores in Q4FY19. The biologics segment growth was led by biosimilar portfolio’s performance of the company in the developed and emerging markets. Although on a QoQ basis the revenue from operations declined by 0.78% from Rs. 1,540.8 crores in Q3FY19 to Rs. 1,528.8 crores.

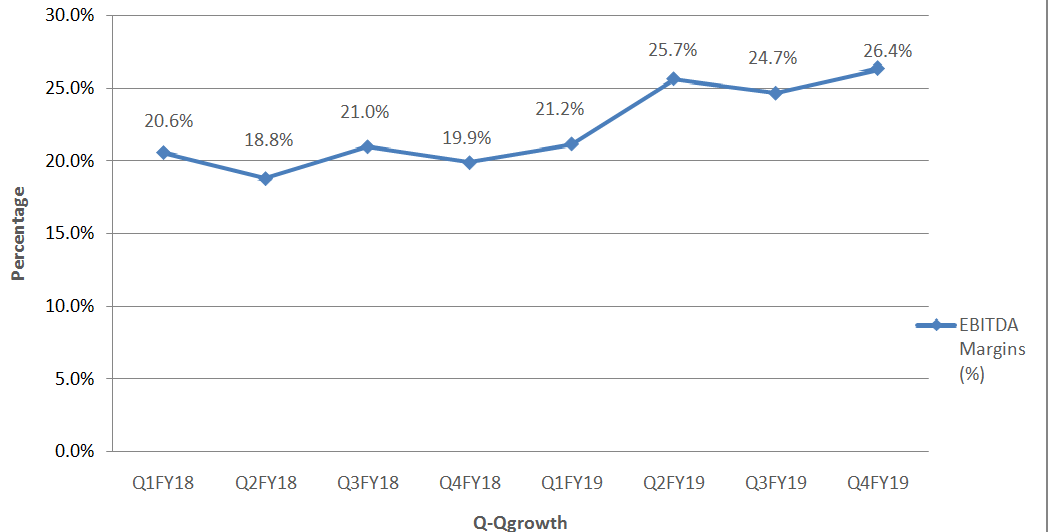

- The EBITDA for Q4FY19 was up by 43% YoY at Rs. 431 crores against Rs. 300 crores in Q4FY18. EBITDA Margins expanded by 400 bps YoY from 24% in Q4FY18 to 28% in Q4FY19. The growth was driven by better product mix this quarter. Core EBITDA (net of licencing, the impact of forex and R&D) margins accounted for 34% for Q4FY19 against 26% in Q4FY18.

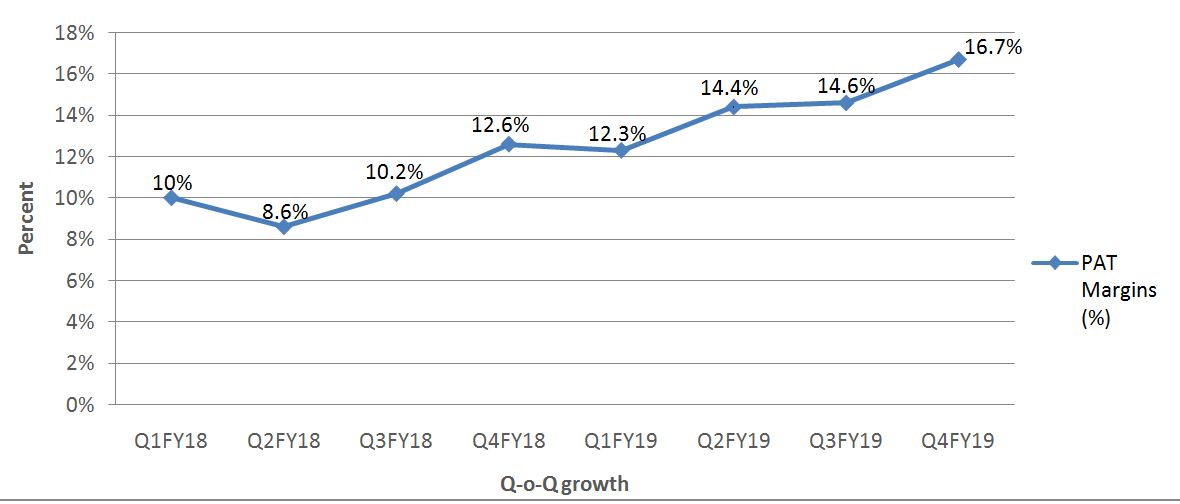

- The adjusted Profit after Tax (PAT) increased for Q4FY19 by 64% to Rs. 214 crores Vs Rs. 130 crores. This was led by robust operational performance and the lower tax rate of 19% this quarter. Net Profit Margin was at 14%.

- Net Research and Development (R&D) cost for Q4FY19 increased by 81% at Rs. 92 crores against Rs. 51 crores same quarter in the previous year. The R&D expenses account for 17% of the revenue for Q4FY19.

- The gross spends increased for Q4FY19 at Rs. 166 crores as compared to Rs. 98 crores for q4fy18. It increased by 70% YoY.

- EBIT margins for the biologics segment has increased from -2% in FY18 to 26% in FY19 on the account of better realisation in biosimilars in developed as well as in emerging markets.

- During the year Biocon’s biosimilar Pegfilgrastim Fulfila gained a market share of 15%-16% in the US this quarter.

- The company booked a forex loss of Rs. 7 crores as compared to a gain of Rs. 42 crores last year.

-

Segmental Performance:

For Q4FY19, the revenue growth was mainly led by biologics (grew by 87% YoY). This segment includes biosimilar, insulin analogs, recombinant proteins, monoclonal antibiotics, encompassing RH-insulin. This segment received approvals and launches in the EU, the US, Australia, Japan and other emerging. Biocon in the last 2 to 3 years invested under this segment

The Biologics segment revenue was driven by robust revenue of its biosimilars Pegfilgrastim and Trastuzumab in Developed and emerging markets. Biosimilar Trastuzumab – Ogivri was launched by Mylan, Biocon’s partner in Europe during this quarter. Furthermore, The Company also launched biosimilar Trastuzumab in other emerging markets in Q4FY19.

Research services, the company’s customs research organisation reported a robust 30% growth on a YoY basis. With the revenue stood at Rs. 534 crores. Syngene in Q4FY19 crossed the 500 crores revenue milestone and a net profit of Rs. 100 crores. The company carters to 331 clients which include 8 out of 10 top global players. The strong performance was buoyed by the performance of discovery services and increased traction in the R&D services.

Small Molecules reported an increased by 11% for Q4FY19 grew on account of generic formulation and steady revenue from its API segment. Small Molecules accounted for 32% of consolidated revenue. The small molecule consists of Differentiated API business and Generic formulations. The company is exploring opportunities with higher profitability in this segment. The performance led in this segment was due to increased traction in immunosuppressants and Statins (Company’s generic formulation drug) sales in the US.

The Branded Formulation segment includes revenue in India and UAE. This segment of faced certain headwinds in UAE due to uncertainty in the UAE market. It includes delays in product registrations and reprising of branded generic products by the Ministry of Health. The Branded Formulation reported negative growth of -11% on a YoY basis in Q4FY19. The company launched Canhera, their first biosimilar Trastuzumab in the UAE in FY19. Canhera is used to enable access to the therapy of breast cancer patients.

- The Board of Directors of the company has approved a final dividend of Rs 1 per share for FY19.

- Further, Biocon on account of 40th Anniversary of the company, it has announced a bonus share in the ratio of 1:1.

Future Outlook:

- R&D outlook: Gross spends as a % of revenue is expected to by 15% by FY20 excluding Syngne. The gross spends will be on biologics, ANDA and novel biologics segment.

- In CY19 Biocon expects the launch of Trastuzumab in the US according to the agreement between Roche and Mylan.

- R&D expenses and depreciation expenses for FY20 is expected to increase significantly. Also, the company’s Employee cost is expected to increase on account of the new set up of biosimilar business under Biocon Biologics.

Valuation:

At CMP of Rs. 621.25, the stock is quoting at a P/E multiple of 51.14x FY20E estimates. The company’s ROE is at 13% and ROA of 4%. The net profit of Biocon jumped 64% YoY led by new launches from biosimilar from across the developed and emerging markets also due to higher margins and effective tax rate in Q4FY19. On a QoQ basis, the company had a marginal decline in the revenue by 0.78% driven by a decline in the branded formulation of UAE business. The company’s R&D and CapEx are expected to increase in the near term. The biologics segment and growth in syngene’s performance are expected to increase the growth for the company. Considering all these factors, we maintain BUY recommendation with a target price of Rs. 716.

| Shareholding pattern | % |

| Promoter & Promoter Group | 60.67% |

| Mutual Funds | 2.86% |

| Foreign Portfolio Investors | 17.90% |

| Financial Institutions | 1.16% |

| Non-Institution | 15.62% |

| Shares held by Employee Trust | 1.43% |

| Non-Promoter-Non Public | 1.43% |

Financial Highlights –

(In crores)

| Particulars | Q1FY18 | Q2FY18 | Q3FY18 | Q4FY18 | Q1FY19 | Q2FY19 | Q3FY19 | Q4FY19 |

| Net Revenues | 933.7 | 968.6 | 1057.9 | 1169.5 | 1123.8 | 1321 | 1570.8 | 1528.8 |

| EBITDA | 192.1 | 182.3 | 221.7 | 233 | 237.9 | 339.6 | 380.7 | 403 |

| EBITDA Margin | 20.6% | 18.8% | 21% | 19.9% | 21.2% | 25.7% | 24.7% | 26.4% |

| Net Profit | 93.6 | 83.2 | 107.4 | 147.6 | 137.9 | 189.8 | 224.9 | 254.6 |

| PAT Margin | 10% | 8.6% | 10.2% | 12.6% | 12.3% | 14.4% | 14.6% | 16.7% |

Net Profit Margin:

EBITDA Margin:

Terms and Conditions:

For more details about financial performance and valuations of companies feel free to contact our research team at contact@equityright.com.

Visit us at www.equityright.com

Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. EQUITY RIGHT will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances.

The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of a specific recipient.

This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks.

The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason.

EQUITY RIGHT accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see the Risk Disclosure Document to understand the risks associated before investing in the securities markets.

Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. Our employees in sales and marketing team, dealers and other professionals may provide oral or written market commentary or trading strategies that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest.

EQUITY RIGHT or its associates might have not received any commission/compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect unless specifically mentioned in the disclosure.

EQUITY RIGHT encourages the practice of giving an independent opinion in research report preparation by the analyst and thus strives to minimize the conflict in preparation of the research report. EQUITY RIGHT or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with the preparation of the research report. Accordingly, neither EQUITY RIGHT nor Research Analysts have any material conflict of interest at the time of publication of this report.

EQUITY RIGHT or its associates collectively or its research analyst do not hold any financial interest/beneficial ownership of more than 1% (at the end of the month immediately preceding the date of publication of the research report) in the company covered by Analyst, and has not been engaged in market making activity of the company covered by research analyst.

Since associates of EQUITY RIGHT are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report.

It is confirmed that equity Right research analysts do not serve as an officer, director or employee of the companies mentioned in the report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject EQUITY RIGHT and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdiction s or to a certain category of investors. Persons in whose possession this document may come are required to inform them of and to observe such restriction.

Research Team:

Sr. Research Analyst – Mr Parag Shah. parags@equityright.com

Research Associate – VarshaK

LEAVE A COMMENT

You must be logged in to post a comment.